Well, 2015 was really quite a year. Brent opened in January at c.$49/bbl, the price having tumbled in Q4 2014; the subsequent rally, which saw it pass $65/bbl, was cut short, and in December, it fell past $37/bbl. Expectations of a brief correction were confounded, and with E&P cuts biting and oil still falling,

offshore seems to be facing a multi-year downturn. But just how does 2015 compare to recent years?

Annus Horribilis

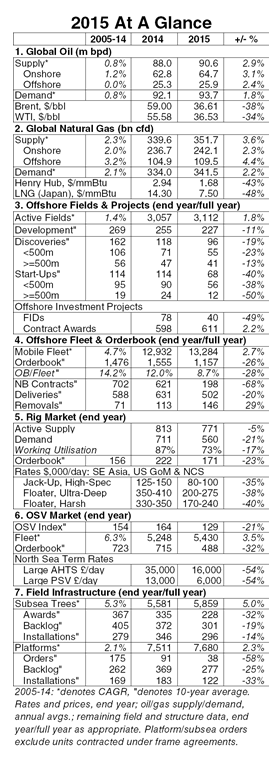

At the end of 2015, Brent stood at around $37/bbl, far below the $60-80/bbl envisaged by many analysts at the close of 2014. Through 2015, various factors conspired to maintain a supply glut and depress the price, including OPEC policy, the resilience of the US shale sector and the softening global economic outlook.

Oil companies reacted to weaker price expectations by cutting E&P budgets and slashing jobs. In the offshore space, oil companies cut E&P spending by around 19% on average. Exploration spending was hit particularly hard, but FIDs at offshore development projects in 2015 were also down approximately 49% y-o-y, as operators were reluctant to commit capital to long lead-time projects. Some offshore areas and fleet segments fared relatively better than others, but 2015 was a pretty bleak year overall.

Turbulent Waters

In terms of offshore field activity, 2015 was the worst year in over a decade. Although some 2015 offshore discoveries like Zohr and Hopkins were notable for their magnitude or fast-track potential, just 96 offshore fields were discovered globally in 2015, down 19% on 2014 and 41% on the 2005-14 average of 162 discoveries per annum.

Meanwhile, only 68 offshore fields started up in 2015, down 41% on both the 114 start-ups of 2014 and the 2005-14 average. In part, this reflected problems pre-dating the fall in the oil price, such as slippage, cost inflation and political risk in countries like Nigeria, Egypt and Brazil. However, due to the paucity of FIDs in 2015, the backlog of fields under development at start 2016 was down roughly 11% y-o-y, even with many planned 2015 field start-ups deferred into 2016 due to slippage. The subsea tree backlog also fell by around 19%, to 301 units.

Challenging Times

The fall-off in offshore field activity compounded developing supply-demand imbalances in the offshore fleet, most notably in the OSV and rig fleets, with an adverse effect on utilization and rates. Thus global rig utilization stood at 73% at end 2015, compared to 87% at end 2014 and 96% at end 2013. Day rates also diminished substantially, with high-spec drillships in the US GoM, for example, commanding $200-275,000/day at end 2015, compared to $600,000/day at the peak of the market cycle. In the OSV sector, falling rig moves and project activity helped depress rates: the North Sea term rate for an AHTS 20,000+ BHP, for instance, averaged $16,800/day, down 52% y-o-y. Moreover, many OSV owners felt compelled to lay up units - a trend still playing out. Offshore newbuild contracting suffered, too with contracting down by 68% on 2014, so that even with delivery delays, the orderbook at start 2016 stood at 1,157 units, down 26% on start 2015.

Troubling Portents

Thus in comparison to the last ten years, and the recent market peak in 2013/14 in particular, 2015 was challenging. The coming year is likely to be a tough one as well, with many energy companies set to make further E&P budget cuts of 20-40% and the oil price seemingly yet to bottom out. The halcyon days of $100+/bbl now seem like a long time ago indeed.

Source: Clarkson Research Services Limited