International Container Terminal Services Inc. (ICTSI) is considered one of the biggest risk takers amongst global container terminal operators. Drewry Maritime Equity Research believes that the company is now showing signs of better risk management that will assist in its long term sustainability.The differential in

expected container volume growth rates between the developed and emerging markets has led operators to focus attention on emerging market opportunities and seek to rebalance their portfolios.

One of the key perceived negatives for ICTSI in the past has been the

geopolitical risks associated in some of its investments in economies

such as Pakistan, Syria and more recently in Iraq that can provide

robust returns. Additionally risks associated with many startups present

another big challenge.

However, DMER believes the company is now following a better risk

management strategy, where it is taking many steps to reduce or

diversify risks. The major steps taken by ICTSI in the recent past are:

1) The company has been partnering with experienced global players in

its terminal start-ups. It recently sold partial interests in the

terminals being developed in Colombia and Nigeria to PSA and CMA CGM,

respectively. Partnering with CMA CGM can also ensure commercial gains

for the Nigerian development.

2) ICTSI has shown interest in investing in less-risky markets. It has

bid for the third container terminal at Melbourne and reportedly shown

interest for the development and operations of the fourth container

terminal at the JN port in Mumbai. It is important however to highlight

here that the company still remains an emerging-market play.

3) By selling partial stakes in assets, the company is reducing risks,

yet maintaining exposure to those assets. ICTSI sold 25% of its interest

(of 100%) in the Nigerian development and half of its interest (of 92%)

in the Colombian development.

Despite these recent moves, DMER expects ICTSI to retain its

expansionist philosophy for the next few years at least. Backing this

up, the company’s Chairman, Enrique K. Razon, Jr., has recently said

that the company intends to quadruple its portfolio to 100 terminals in

the next 25 years.

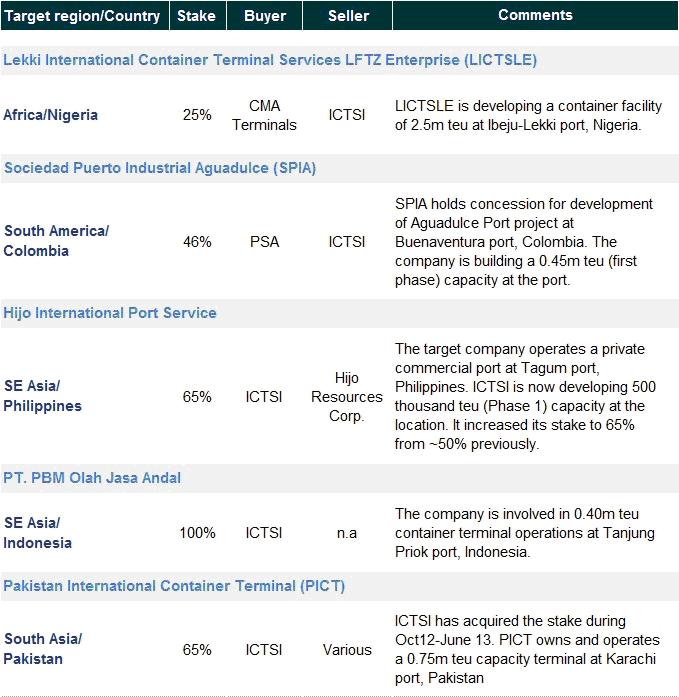

Table 1

Recent M&A Activity by ICTSI

Source: ICTSI, DMER

Source: ICTSI, DMER

DMER believes that a large component of the risk management strategy

adopted by ICTSI can be termed as portfolio management, which is not new

among container terminal operators. The most fitting example in DMER’s

coverage universe is that of DP World, which in the recent past has sold

its terminal interests in Hong Kong and Vostochny (Russia’s Far East)

and is focusing on developments at Jebel Ali and London Gateway. The

company has reportedly shown interests in new terminal investments in

Bangladesh and India. APM Terminals, part of the A.P. Moller-Maersk

group, also recently sold its 24% interest in the APM terminal Zeebrugge

and at the same time is expanding in faster-growing geographies such as

Russia (through its investment in Global Ports Investments). The

company has a number of planned investments in Africa, a region which is

expected to experience strongest growth in container volumes in times

to come.

Global terminal operators owning partial stakes in assets is also fairly

common trend in the industry. Large global operators such as HPH, DP

World and APM Terminals have considerable differentials between total

throughput and equity throughput handled. For 2012, HPH, DP World and

APM Terminals handled 74.3m, 54.5m and 59.7m teu, respectively, while

their equity throughput stood at only 44.8, 33.4 and 33.7m teu,

respectively. Drewry defines equity throughput as throughput adjusted

for percentage stake held at a terminal. For example if an operator has

30% stake in a terminal, only 30% of the volumes handled by that

terminal will be considered for arriving at the total equity throughput

of the operator.

Partnering with shipping lines in terminal investments is also prevalent

among mature operators. Apart from group-level relations of many

terminal operators with shipping lines, large independent global

operators have common ownership with shipping lines at various terminal

assets.

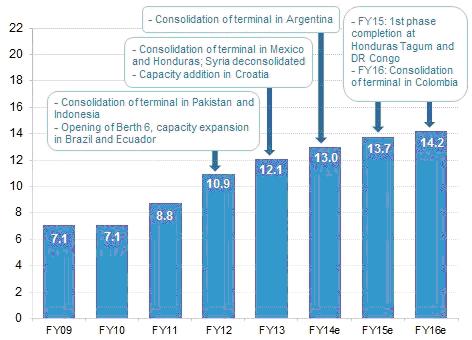

Figure 1

Growth in Handling Capacity by ICTSI (M teu)

Source: ICTSI, DMER

Source: ICTSI, DMER

Africa is one of the key markets that ICTSI is targeting. In line with

this strategy, the company recently announced the formation of a joint

venture (with 60% interest) to develop and operate a river multipurpose

terminal (with a container terminal) along the banks of the Congo River

in Matadi, Democratic Republic of Congo. In the first phase, the JV

plans to develop a 120,000 teu capacity terminal to be ready in 18-24

months. We believe that the location of the proposed development is

reasonably strategic as it can feed the Kinshasa market (capital city)

with consumer goods. Among the most recent development the company has

announced to develop first phase capacity of 300,000teu at Port of Umm

Qasr in Iraq. On full development the facility is expected to have 600

meters of quay with 900,000teu of capacity.

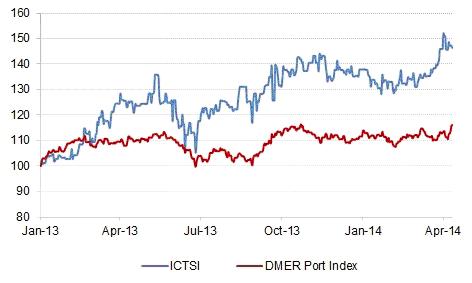

Figure 2

ICTSI Stock Outperformance Compared to DMER Port Index

Source: Bloomberg, DMER

Source: Bloomberg, DMER

ICTSI’s share price has had a spectacular run in 2013 registering a

growth 40% during the year. During the period DMER’s Port Sector Index

has registered a growth of only 14%. DMER in March 2014 upgraded its

fair value on ICTSI stock to PHP 109 from PHP 83 previously. The stock

currently trades near our fair value target.

• Our View

ICTSI will perhaps remain as one of the most aggressive amongst global

container terminal operators in times to come. It is one of the players

targeting highest ROI’s from its investments. However what is heartening

to see is company’s practical approach towards reducing/diversifying

some of the risks.

Source: Drewry Maritime Research (www.drewry.co.uk/ciw)