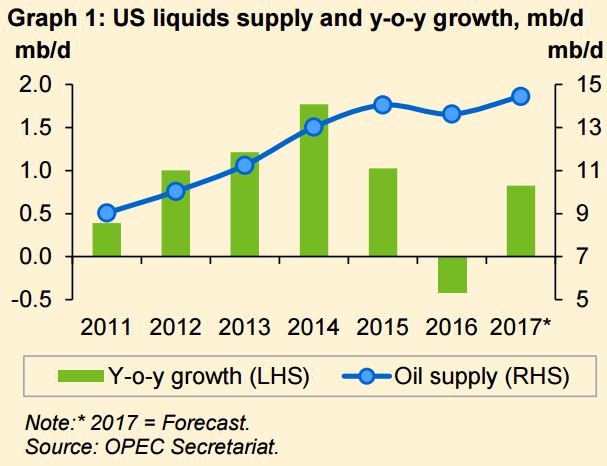

Low oil prices in 2016 led to a reduction of around 23% in global E&P investments compared to the previous year, together with the deferral of several upstream projects. Particularly in North America, E&P spending fell by around 38%, as observed in the 48% y-o-y decline in US rig counts, as well as lower well completions. Non-OPEC oil supply decreased sharply in 2016, contracting by 0.7 mb/d from the high growth of 2.3 mb/d in 2014 and 1.5 mb/d in 2015. Non-OPEC supply in 2016 saw contractions in OECD Americas (0.5 mb/d), China (0.3 mb/d), and Latin America (0.1 mb/d), while an increase was seen in the FSU (0.2 mb/d), driven by robust output from Russia. The oil supply contraction in OECD Americas in 2016 was mainly due to US onshore crude oil output which includes tight oil, along with annual declines in Mexico and outages in the Canadian oil sands. US oil production showed a y-o-y decline of 0.4 mb/d in 2016, but this trend has reversed so far in 2017, primarily due to higher oil prices together with cost cuts (Graph 1).

The non-OPEC supply performance in 2017 will depend on many factors, including the world economy; higher spending by oil companies, particularly in North America; new economic and energy policies in major economies, especially the US; and the timely implementation of oil projects in Canada and Brazil, as well as oil price developments and to some extent geopolitics. US oil and gas companies have already stepped up activities in 2017 as they start to increase their spending amid a recovery in oil prices. As a result, US crude oil production surpassed 9 mb/d in February 2017, about 0.5 mb/d higher than the low seen in September 2016. For 2017, total US liquids production is forecast to increase by 0.82 mb/d with crude oil contributing 0.6 mb/d. In the first two months of this year, tight crude output increased by 0.10 mb/d from December 2016, while NGLs output rose by 0.26 mb/d over the same period.

With the pick-up seen in drilling activities, as well as increased cash flows, US tight crude output is expected to rise rapidly and increase by 0.6 mb/d in 2017. Overall, non-OPEC supply in 2017 is expected to increase by 0.95 mb/d. In addition to the growth in the US, higher oil production is expected in Canada (0.22 mb/d) and Brazil (0.21 mb/d), while Mexico and China are forecast to see the largest contractions (Graph 2).

A large part of the excess supply overhang contained in floating storage has been reduced and the improvement in the world economy should help support oil demand. However, continued rebalancing in the oil market by year-end will require the collective efforts of all oil producers to increase market stability, not only for the benefit of the individual countries, but also for the general prosperity of the world economy.

Source: OPEC