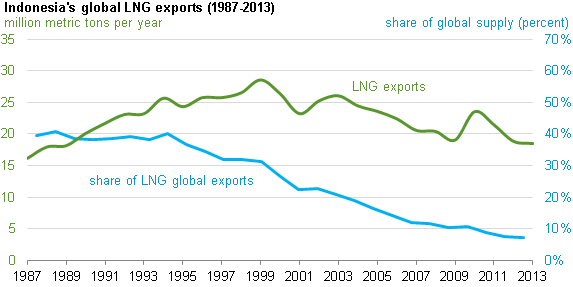

After

accounting for more than one third of global liquefied natural gas

(LNG) exports throughout the 1990s, Indonesia's share of the global

market is currently about 7%. This declining share is a result of both

growing global LNG demand that is increasingly served by non-Indonesian

supply and lower Indonesian exports. While

Indonesia's LNG exports have

fallen by 40% since 1999—driven by the country's economic growth that

has stimulated higher levels of domestic energy consumption,

particularly of natural gas—global LNG demand has risen over 150% during

the same period.

Source: U.S. Energy Information Administration, PFC Energy

Source: U.S. Energy Information Administration, PFC Energy

Until 2006, when its share was overtaken by

exports from Qatar, Indonesia was the largest LNG exporter in the world.

Indonesia is now the fourth-largest exporter of LNG after Qatar,

Malaysia, and Australia, according to EIA estimates. Indonesia exported

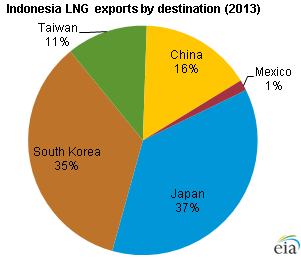

nearly all of its LNG to South Korea, Japan, China, and Taiwan, with

much smaller volumes to Mexico and a few other nations. In 2013,

Indonesia exported approximately 818 Bcf of LNG.

Source: U.S. Energy Information Administration, PFC Energy

Note: Does not include LNG sent to regasification plants in Indonesia

LNG exports are

politically sensitive in Indonesia because of increased domestic demand

for energy. Expected growth in natural gas demand led the government to

pursue policies securing domestic supplies for the local market. To meet

the natural gas domestic market obligation (DMO), LNG producers must

designate 25% of supply for the domestic market.

Indonesia

currently has three liquefaction plants—Arun, Bontang, and Tangguh—on

the islands of Sumatra, Kalimantan, and Papua, respectively. IHS Global

Insight estimates current total liquefaction capacity at roughly 1.5

trillion cubic feet (Tcf) per year. Two new liquefaction plants,

Donggi-Senoro and Sengkang, are under construction in Sulawesi. The

Donggi-Senoro LNG plants received government approval only after the

developers designated 30% of the output explicitly for domestic

consumption, exceeding the DMO floor of 25%.

As part of its

efforts to meet domestic demand, Indonesia is planning additions to its

regasification capacity. PT Pertamina (the country's state-owned energy

supply company) plans to convert the Arun LNG plant into a

regasification terminal to serve the domestic market. IHS Global Insight

expects the converted Arun plant to come online by late 2014 with a

capacity of roughly 146 Bcf per year. In addition, Pertamina and PLN

(Indonesia's state electricity firm) plan to develop eight small LNG

receiving terminals in the eastern regions of the country by 2015, with a

total capacity of 67 Bcf per year. The government intends for these

facilities to supply domestic electricity plants.

In December

2013, Indonesia signed its first gas import contract with Cheniere

Energy (United States) to receive 38 Bcf per year of LNG for 20 years

from the planned Corpus Christi liquefaction terminal, located in the

Gulf Coast of the United States, starting in 2018.

Source: EIA