The ongoing energy transition combined with the effects of Covid-19 will drive future oil demand to lower levels than what was expected just months ago. As a result, a plethora of planned refinery additions will far exceed closures towards 2025, and utilization rates will likely never recover to pre-pandemic levels unless some capacity closes early, a Rystad Energy market analysis reveals.

New and expanding projects from the beginning of 2020 and up until the end of 2025 are estimated to add about 13 million bpd of global capacity as Asian and Middle Eastern refiners complete scheduled expansions and new builds. Meanwhile, a surge of capacity closures will reach only about 3 million bpd, a relatively small number compared to additions.

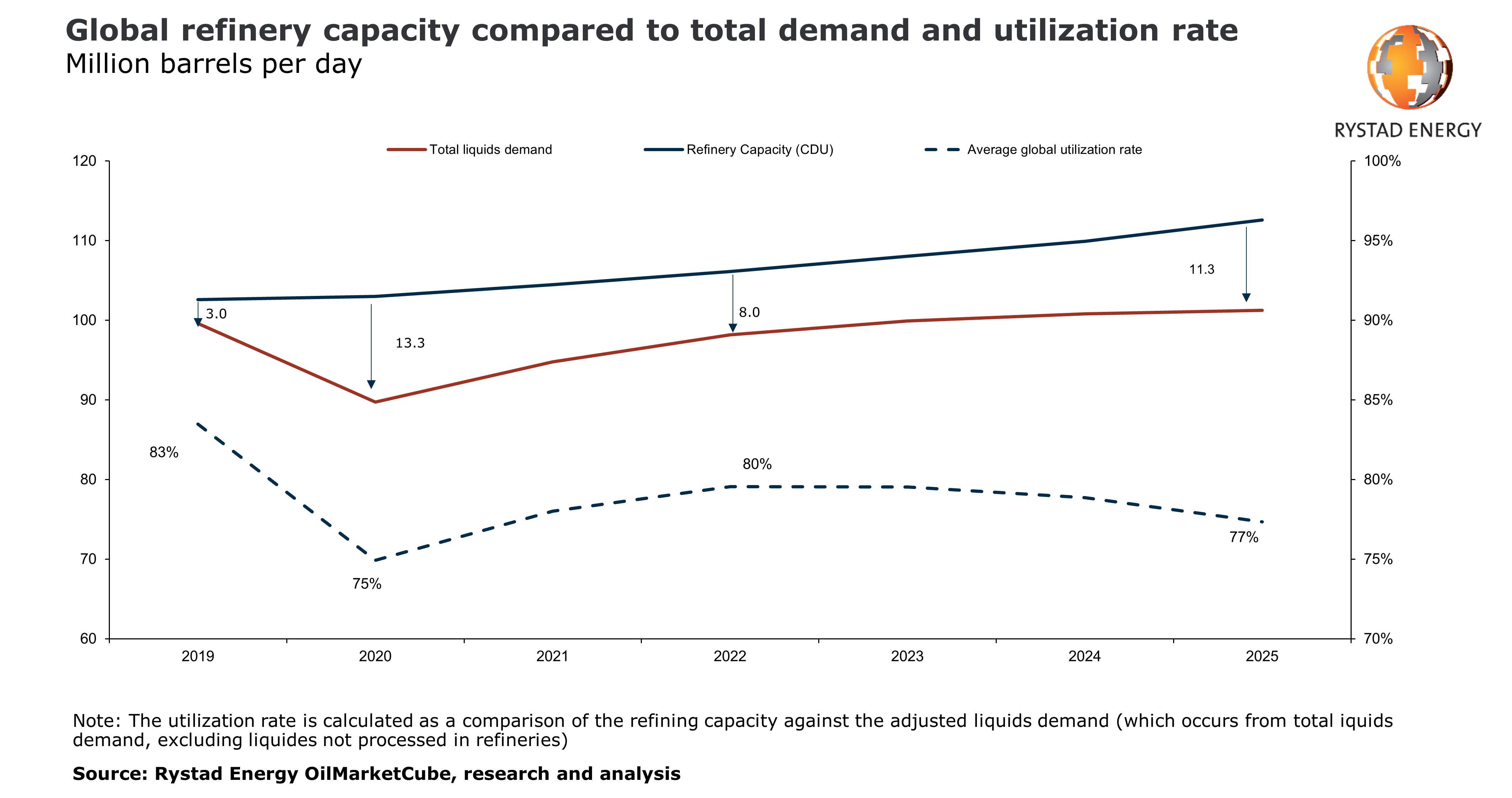

This means that net refining capacity additions will reach 10 million barrels per day (bpd) between the beginning of 2020 and the end of 2025 – an increase that oil demand will never be able to cover, even when the effect of Covid-19 becomes a thing of the past.

In 2020, Rystad Energy projects a net growth of approximately 400,000 barrels per day (bpd). As a result, global refining capacity will be driven to 103 million bpd this year from 102.6 million bpd in 2019. With oil demand plunging in 2020, adjusted liquids demand will only reach 77.2 million bpd, causing utilization* to drop to a low of 75% for the year from 83% in 2019.

As oil demand grows from 2021 onwards, refinery capacity utilization will too, reaching 78% in 2021 and peaking at 80% in 2022 and 2023. From that point, oil demand growth rates will fall behind those of refinery capacity additions and utilization will consequently fall and reach 77% in 2025.

“As oil demand will likely peak a couple of years after 2025, if not earlier, for utilization to rise again, the least efficient and most poorly-located refinery capacity is doomed to close. A long period of rationalization is ahead of us if we are ever to return to pre-Covid utilization rates and margins,” says Julie Torgersrud, Oil Markets Analyst at Rystad Energy.

The year has been a devastating one for refiners, as historical overcapacity was accompanied by a drop in global fuel demand, slashing margins and forcing already struggling refineries into early retirement. So far in 2020, 28 refineries have announced closures. Our analysis shows that permanent capacity reductions in 2020 will surpass 1.0 million bpd, while more closures loom given the additional idled capacity awaiting final decisions.

The bulk of announced shutdowns will take place in mature markets like Europe, North America and Japan, where 12 facilities are expected to close before the end of 2021. Asian refineries are also victims to the changing refinery climate and are expected to remove over 1.0 million barrels of daily refining capacity by 2021. 50% of Asian capacity closures stem from China, which has 550,000 bpd of announced closures from less-efficient, independent teapot refineries to make way for the giant Yantai refinery complex in the Shandong oil hub.

We expect idled refinery capacity to exceed 950,000 bpd in 2020 as the recovery in fuel demand remains sluggish. 760,000 bpd of globally idled capacity stems from closed refineries in North America and Europe, while five refineries on the American Atlantic coast remain mothballed in the third quarter of 2020. Idling capacity was a hurried response to the declining fuel demand, as temporarily shutting unprofitable refineries proved more economical than continuing to operate on already tight margins.

Capacity additions in 2020 are estimated to add 1.4 million bpd despite the tough economic climate for refiners. We then expect an additional 6.9 million bpd until the end of 2023, leading to a net capacity increase of roughly 5.4 million bpd for the 4-year period.

Between 2019 and 2025, the discrepancy between global refining capacity and total liquids demand will increase by 8.1 million bpd to a gap of over 11 million bpd.

Significant capacity additions in regions traditionally relying on product imports, like South-East Asia, could render these nations to become net exporters. Consequently, refiners in high-cost regions like Europe and Australia would be squeezed out of the market, which would accelerate the rate of refinery closures in these regions.

*The utilization rate is computed as the ratio between our adjusted liquids demand and refinery capacity, instead of the usual crude intake over refinery capacity.

Source: Rystad Energy