The recent decline in crude oil prices has created the potential for

weaker crude oil production. EIA's Drilling Productivity Report (DPR)

includes indicators that provide details on the effect low prices may

have on tight oil production, which accounts for 56% of total U.S. oil

production. Analyzing these indicators and the

changes in oil production

following the drop in crude oil prices during the 2008-09 recession may

offer some insight into possible near-term oil production trends.

Source: North Dakota Department of Mineral Resources, Bloomberg

The

price of West Texas Intermediate (WTI) crude oil delivered to Cushing,

Oklahoma declined more than 31% from June to November 26 and another 7%

after the late November announcement of the Organization of the

Petroleum Exporting Countries (OPEC) decision to maintain the current

production level. At $60 per barrel, the current price of oil is likely

approaching or already below the expected per-barrel costs of some of

the most expensive U.S. tight oil projects.

Some of the most

active production fields in the country are in North Dakota. Indicators

tracked by the DPR and North Dakota's Department of Mineral Resources

(DMR) cover much of the exploration and production process, from

planning to production. These indicators include:

• Permits. Before

drilling begins, producers must sign lease contracts and apply for

permits to drill exploration and development wells.

• Rig movement. Drilling rigs must be secured and moved to permitted locations.

• Spuds. Spudding is the term for the ground-breaking process of a new

drilling project. In North Dakota, the spud count is a count of new

wells drilled.

Based on the most recent data released by North

Dakota's DMR, drilling and production activities in the state have not

slowed, despite the significant decline in domestic crude oil prices

since July 2014. Oil production in September 2014—the latest data

available—rose 5% from the prior month.

The number of permits

issued in October 2014 was 28% above the September level, but it dropped

30% in November. However, when normalized based on the number of

business days during those months, October is only 17% above September's

level, and November is only 10% lower than October.

Source: North Dakota Department of Mineral Resources

Although

the current economic situation is fundamentally different from the

recession of 2008-09, changes in oil prices, production indicators, and

production volumes during the recession may offer insight into what may

happen next with U.S. shale oil production.

Source: North Dakota Department of Mineral Resources, Bloomberg

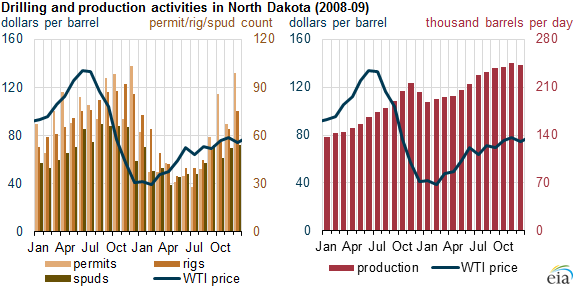

During

the 2008-09 recession, monthly average WTI prices fell by 71% to $39.09

per barrel between June 2008 and February 2009. At the time, shale oil

production in North Dakota was still in the testing phase and thus

relatively expensive. Drilling and production continued to increase

until November 2008, when WTI prices dropped below $57 per barrel. Below

$57 per barrel, the number of projects that were interrupted increased

significantly, with the number of permits declining 73% from December

2008 to July 2009, the number of rigs declining 62% from November 2008

to May 2009, and the number of spuds declining 55% from November 2008 to

April 2009. However, the decline in production was not nearly as

dramatic, falling only 13% from November 2008 to January 2009, after

which time production began increasing.

Looking forward, EIA

expects 2015 drilling activity to decline as a result of less-attractive

economic returns in some areas of both emerging and mature oil

production regions. Many companies will redirect investment away from

marginal exploration and research drilling and into core areas of major

tight oil plays. However, projected oil prices remain high enough to

support development drilling activity in the Bakken, Eagle Ford,

Niobrara, and Permian Basin, which contribute the majority of U.S. oil

production growth.

EIA expects U.S. crude oil production to

average 9.3 million barrels per day (bbl/d) in 2015, up 0.7 million

bbl/d from 2014, but down from expected growth of 0.9 million bbl/d in

last month's Short-Term Energy Outlook. However, all of the decrease in

forecast production growth comes in the second half of 2015. EIA revised

production growth downward by 140,000 bbl/d and 270,000 bbl/d in the

third and fourth quarters, respectively, compared with the previous

forecast. However, this forecast remains particularly sensitive to

actual prices available at the wellhead and drilling economics that vary

across regions and operators.

Source: EIA